A Simple Governance Framework for Small to Mid-Sized Law Firms

Sean LarkanI am quite frequently asked for advice on what the ‘ideal structure’ is for the typical governance set-up in a small to mid-sized firm. By “governance set-up”, we mean the leadership, management and decision-making structure of the firm; who or which body is responsible, is accountable and has the authority to do and decide on various matters.

Some initial research and discussion with existing leadership will determine how one should tackle this in a particular firm:

- What is the existing leadership, management and decision-making structure, and how is that viewed as functioning? For instance, is there a managing partner or general manager in place? Is there a board and/or some form of executive or management committee? Are managers or partners in charge of client-service and support-service areas?

- What are present expectations around contributions by partners – e.g., covering items such as financial performance, financial management of own practice and teams, business building and marketing, client-relationship management, brand building, building the firm’s capital fabric, or people management, to name a few?

- How hands-on or hands-off are the partners presently in relation to management and decision-making? What level of communication do they feel they need? What is their thinking in this regard?

- What is the present positioning of the firm in its market, and does it have a clear vision and strategy? Is it in a strong position, facing big challenges or wanting to grow, and so on?

- What is the culture of the firm and what are the engagement levels of staff and partners?

I have found from personal experience running mid-size to large firms for twenty years, and consulting to such firms for the past decade, that:

- It is more helpful to think in terms of having a flexible governance framework than a governance structure as such. One can use the framework to deal with the needs of a large majority of firms, each with a slightly different make-up and priorities;

- Given the large number of diverse challenges and the important types of contributions expected of partners to succeed in practice today, one should ideally wean them off being involved in all decisions and firm management, especially those matters relating to day-to-day management.

With the above in mind, I have found the following framework and simple set of guiding principles worthy of consideration:

- Start by reserving a limited number of strategically important topics (e.g., exiting a partner) for decision-making by the owners/equity partners;

- If necessary, reserve some items to be signed off by the partnership as a whole, but only once the board (see below) has already signed off on them, such as firm-wide strategy, annual income and expense budget, a new lease, and the like. Instead have partner meetings focus on practice-group and industry-sector strategies and business-building initiatives, in each case under the direction of the practice group or industry sector leader. Partner meetings should also be a forum for communication by the managing partner, senior managers, practice and industry sector heads, and so on;

- Reserve a small number of items (so-called “strategic matters”) for board or management committee attention/decisions. If it is decided to have a management committee or board, preferably have just a board (and keep it as small as you can get away with, and elected), not both a board and a management committee; otherwise, confusion invariably reigns and this will lead to frustration for a managing partner or CEO;

- On the support-services side (IT, human resources, marketing and brand, finance and information management) when a firm can justify it, I suggest dedicated, highly capable managers be appointed for each area, reporting to the managing partner. As the firm grows, consideration can be given to appointing a general/practice manager who would then take on oversight of other support-service managers. A variation on this theme, which I don’t encourage, but which has worked for some of my clients, is to have an interested/qualified partner in charge of each area;

- Below that, if a managing partner or CEO is the right person, they should be responsible/accountable for the rest, with a communication/consulting/delegation-upwards role vis à vis the board.

This makes for quite a simple, short governance structure with built-in flexibility. The benefit is that the structure is clear to everyone, and everyone knows where the buck stops: where responsibility lies, and who is accountable. I have seen this work very well, in slightly varying forms, in three firms I ran and also many to which I have consulted. It can be tweaked from year to year on review to suit changing needs or circumstances.

This simple solution avoids the need for drafting lengthy and detailed governance documentation covering all aspects of decision-making at different levels of authority and so on; in reality, these documents usually get settled after countless meetings and hours of discussion, sometimes involving the whole partnership, only to gather dust in some filing cabinet and seldom be consulted. Obviously, some firms might need or want to have more detail determined upfront about some areas of the above framework; one such example is the powers and duties of a management committee. These should be the exception rather than the rule.

For some, such frameworks take some getting used to as they keep partners from getting involved in day-to-day management and interfering in a lot of things! However, as noted above, there is so much for partners to get on top of nowadays they shouldn’t have time to get into this anyway.

The Focus Challenge – Part I: Your Practice

Gerry Riskin1. Substantive Practice

Gone are the days when some level of specialization in an area could sustain a practice over a lawyer’s lifetime. Things are changing too fast and new competitors will emerge – some of them not even law firms.

In the meantime, what you can do is think about the future of both your practice area and the clients you serve.

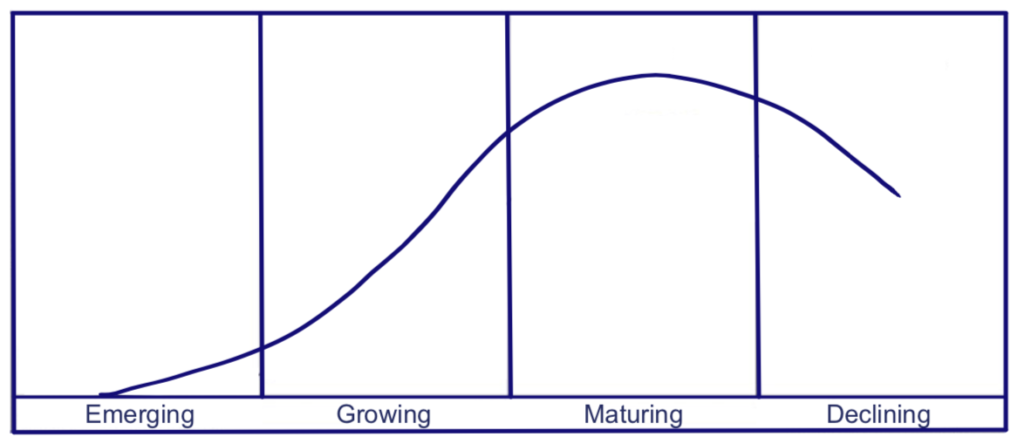

We’ve been using this life cycle S-curve for a long time. It was borrowed from industry and the legal profession has embraced it gradually over the last number of decades. The graph applies to both your substantive practice, and the client you serve within it.

The S-curve may be applied to your practice, your firm, your practice area, your client, an industry, or all of the above. Most work gravitates to the right side of the curve where rates are low and competition is high, as opposed to the left where exciting emerging areas afford major strategic opportunities with few competitors and low resistance to fees. Therefore, it is necessary to be forward-thinking.

2. The Business of Law in a Digital World

I am asked by people at international associations of law firms, and sometimes by those at individual firms, “How is the practice of law changing? What do I need to know, and how do I keep up?”

The oldest members of your firm might remember when firms began to use computers for data-processing. All lawyers will remember the accelerating change of technology — from how word-processing is done to how documents are generated.

Today, with machine learning and what is commonly referenced as “artificial intelligence,“ the quality of documentation is ever-enhanced, while the cost of generating it decreases.

Many firms seem unaware that they now exist in a digital environment that needs to be nurtured. Firms are now rated on-line whether they like it or not, and enlightened firms are fostering more positive reviews.

This is not the place for a deep dive on the subject, but it is a caution that firms that are not making a considerable effort to learn the changing technology around them – and to embrace it – will soon be left behind.

3. The Firm

Well-managed firms outcompete poorly managed firms. Firms with a business plan outcompete firms without a business plan. Why then, at conferences where managing partners gather, do we see by the use of anonymous voting machines that the vast majority of firms don’t have a business plan? (I’m referring to a sample across a wide spectrum of firm sizes. If you’re thinking that the top 25 firms in the world likely have a plan, you are correct.) Firms that do not see the benefit of managing the business of law are being left behind.

The better firms train their leaders on how to get improved performance from their people. The better firms train their individual lawyers on client-relations skills so they can give greater satisfaction to their clients and attract more desirable work, both in traditional ways (via personal relationships) and in digital ones (through an online presence).

I’d be happy to discuss any of the component pieces of this article in greater depth as a courtesy to my readers. Contact me at edge.ai or at my blog, gerryriskin.com.

In the next two parts of this series of articles, I will be touching on: